Whether you’re a first home buyer, reviewing your existing mortgage or a property investor, we connect you with expert mortgage advisers who work hard to find the right deal. In most cases, adviser services won’t cost you a cent.

Thinking about refinancing your mortgage? You're not alone. Thousands of Kiwi homeowners are making smarter financial moves by exploring their refinancing options – often saving tens of thousands of dollars in the process.

More New Zealanders are choosing to work with an advisor, rather than deal directly with a lender, because it saves them time and helps to ensure they pay less interest.

We work with multiple lenders, giving you access to more options and competitive rates. Our team handles the hard work, providing personalised advice and support from start to finish.

Yes. Buying your first home may be more achievable than you think. Eligible buyers could secure a home loan with as little as a 5% deposit through available lending options. Our mortgage advisers can assess your eligibility and guide you through the process.

Your borrowing capacity depends on your income, expenses, deposit, and credit history. A mortgage advisor will run the numbers, explain what lenders are likely to approve, and make sure there are no surprises later.

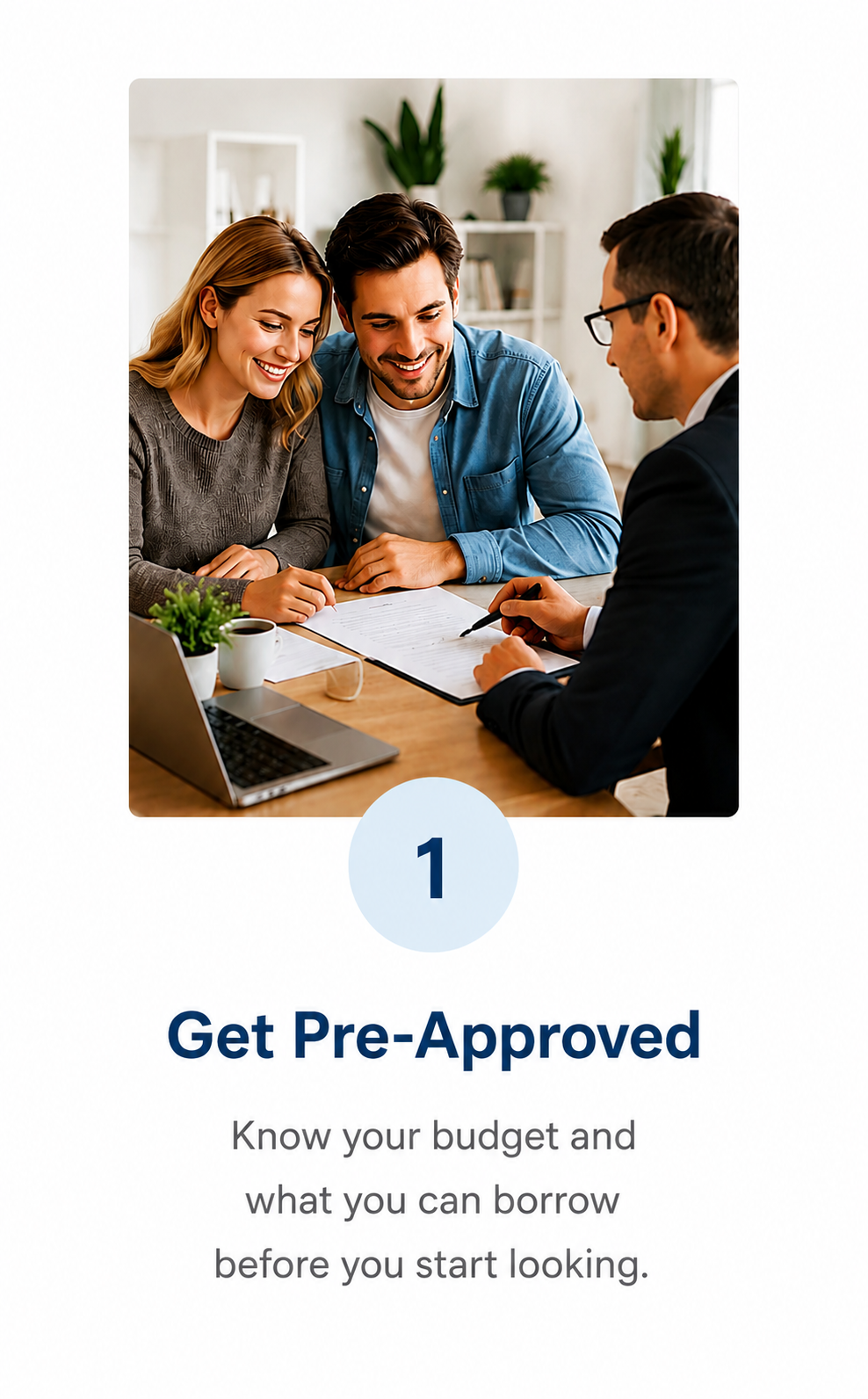

Pre-approval is a conditional agreement from a lender to lend you up to a set amount, based on your financial position at the time of application. You don't legally need it, but it makes everything easier. You'll know your budget before you start looking, you can move quickly when you find the right property, and sellers take you more seriously. Most advisors recommend getting pre-approval sorted before you start attending open homes.

An offset mortgage links your savings to your home loan, helping reduce the interest you pay. The more savings you hold, the less interest you'll be charged on your mortgage balance.

Your deposit is only part of the picture. It's important to budget for additional expenses such as legal fees, property reports, insurance, moving costs, council rates, and any immediate repairs or maintenance. Having a financial buffer can help make your home-buying journey smoother and less stressful.